Asian equities will open Tuesday with support from a rally on Wall Street amid optimism that the Federal Reserve will pause its most-aggressive tightening campaign in decades.

Futures for Japanese and Australian shares rose while those for Hong Kong fell slightly. Contracts for US benchmarks were marginally higher in Asia after the Nasdaq 100 and the S&P 500 closed at the highest levels since April 2022.

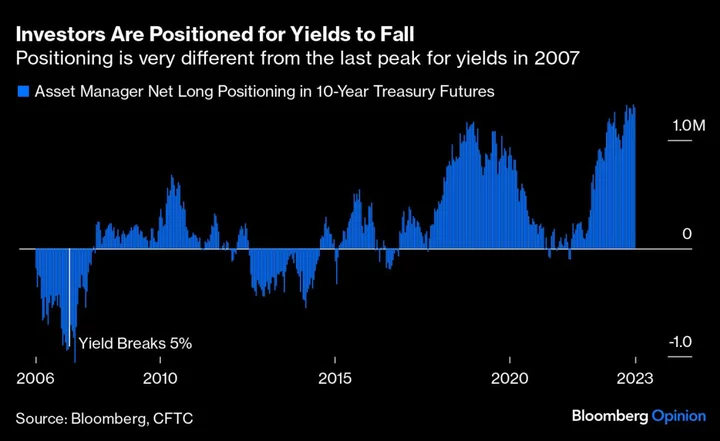

Treasury two-year yields, which are more sensitive to imminent central bank moves, edged lower Monday. The Bloomberg Dollar Spot Index was little changed.

All eyes are on the Federal Open Market Committee, which is expected to keep interest rates in the 5%-5.25% range on Wednesday. This assumes consumer price index data later Tuesday shows subdued inflationary pressure. The likelihood of a hike is higher in July, with swaps showing an almost quarter-point of additional tightening priced in by next month’s meeting.

Traders in Australian markets, which are reopening after a holiday, will be looking to consumer confidence data amid concerns that aggressive monetary-tightening could trigger a recession.

Sentiment toward Chinese assets remains week. Goldman Sachs Group Inc. analysts said the nation’s struggling real estate industry is expected to see an L-shaped recovery in the coming years. They also downgraded earnings estimates and price targets on some Chinese property stocks.

Goldman also cut its oil forecast for the third time in six months, sending West Texas Intermediate more than 4% lower to its lowest close in three months. Even with Saudi Arabia’s decision less than two weeks ago to cut 1 million barrels a day of production, the bank sees crude supplies swelling, and trimmed its year-end price estimate to $86. WTI was marginally higher in early Asian trading.

On Monday, Tesla Inc. climbed for a 12th straight session — a record winning run — and Apple Inc. hit an all-time high. KeyCorp and Citizens Financial Group Inc. led losses in banks after disappointing updates at an industry conference.

Oracle Corp. gained as its sales beat estimates, signaling the software maker’s cloud business is benefiting from demand for artificial intelligence workloads. Meanwhile, Bitcoin dropped as last week’s regulatory crackdown by the US Securities and Exchange Commission weighed on sentiment.

Prospects for a pause in rate hikes helped the S&P 500 enter a bull market last week, with the gauge surging over 20% from its October low. Wall Street’s top strategists are split on the way forward.

To David Kelly, chief global strategist at J.P. Morgan Asset Management, the Fed should weigh progress on inflation against the risk of recession in its June meeting.

“The numbers just won’t support any further tightening, and this will become clearer in the next few weeks,” Kelly said. “If so, the investment environment could support lower long-term interest rates, a lower dollar and further gains in stock prices.”

A “hawkish skip” would only buy the Fed a little bit of time, according to Neil Dutta at Renaissance Macro Research.

“If the Fed decides to skip the June meeting, as I anticipate, I don’t think they have a choice but to sound hawkish given their data-dependent pledge,” Dutta added.

Key events this week:

- US CPI, Tuesday.

- Eurozone industrial production, Wednesday.

- US PPI, Wednesday.

- Federal Reserve rate decision, updated economic forecasts, Jerome Powell’s press conference, Wednesday.

- IEA oil market report, Wednesday.

- China property prices, retail sales, industrial production, Thursday.

- China central bank meeting to decide on one-year policy loan rate, Thursday.

- European Central Bank President Christine Lagarde holds press conference following the rate decision, Thursday.

- US initial jobless claims, retail sales, empire manufacturing, business inventories, industrial production, Thursday.

- Bank of Japan rate decision, Friday.

- US University of Michigan consumer sentiment, Friday.

Some of the main moves in markets:

Stocks

- S&P 500 futures were little changed as of 7:26 a.m. Tokyo time. The S&P 500 rose 0.9%

- Nasdaq 100 futures rose 0.1%. The Nasdaq 100 rose 1.8%

- Nikkei 225 futures rose 0.8%

- Australia’s S&P/ASX 200 Index futures rose 0.4%

- Hang Seng Index futures fell 0.2%

Currencies

- The euro was little changed at $1.0760

- The Japanese yen was little changed at 139.56 per dollar

- The offshore yuan was little changed at 7.1554 per dollar

- The Australian dollar was little changed at $0.6753

Cryptocurrencies

- Bitcoin was little changed at $25,894.45

- Ether rose 0.1% to $1,741.29

Bonds

- The yield on 10-year Treasuries was little changed at 3.74%

Commodities

- West Texas Intermediate crude rose 0.4% to $67.36 a barre

This story was produced with the assistance of Bloomberg Automation.

--With assistance from Rita Nazareth.