Underlying US price pressures are seen advancing at a pace that backs apprehension among Federal Reserve officials to signal the all-clear in their inflation-fighting efforts.

The consumer price index excluding food and fuel, a measure favored by economists as a better indicator of underlying inflation, is seen increasing 0.3% for a third month.

Compared with October of last year, the core CPI is projected to rise 4.1%. That would match the annual advance in September and snap a six-month stretch of slowing price growth.

While considerable progress has been made since hitting a multi-decade high a year ago, the pace of inflation remains elevated and above the Fed’s goal. Having paused tightening at consecutive meetings, leaving the benchmark rate at a 22-year high, policymakers are proceeding deliberately — and not ruling out further increases.

“If it becomes appropriate to tighten policy further, we will not hesitate to do so,” Chair Jerome Powell said Thursday. “We will continue to move carefully, however, allowing us to address both the risk of being misled by a few good months of data, and the risk of over-tightening.”

Read More: Powell Says Fed to Be Careful, Won’t Hesitate to Hike If Needed

Central bankers slated to speak in the coming week include Chicago Fed President Austan Goolsbee and Fed Governor Philip Jefferson.

Tuesday’s CPI report is the first of a heavy slate of US indicators that will provide a glimpse into the economy’s performance at the start of the fourth quarter. Retail sales data on Wednesday are projected to show that consumers dialed back their spending in October after a string of solid monthly advances.

Reports later in the week are likely to show declines in industrial production and housing starts.

Looking north, Canadian will release home sales data for October after prices slipped in September for the first time in six months, weighed down by higher rates.

What Bloomberg Economics Says:

“In our view, Fed officials will most likely retain a tightening bias until monthly core CPI is running at a consistent 0.2%-0.3% pace for at least six months. The low end of that range only happened for a summer, and core CPI has been creeping toward the upper end since, which is more consistent with an annual rate of 3% inflation than 2%.”

— Anna Wong, Stuart Paul, Eliza Winger and Estelle Ou, economists. For full analysis, click here

Elsewhere, Chinese economic reports, data possibly showing a contraction in Japan, slowing UK inflation, and new regional forecasts from Europe will be among the highlights.

Click here for what happened last week and below is our wrap of what’s coming up in the global economy.

Asia

APEC meetings are held all week, with US President Joe Biden and Chinese leader Xi Jinping set to meet in San Francisco in an event likely to be closely watched by investors globally.

China on Wednesday is expected to hold its one-year medium-term lending facility rate at 2.5%, and report on a range of data from industrial production to retail sales, giving the latest snapshot into the state of the world’s second-largest economy.

The same day, Japan’s third quarter gross domestic product data is forecast to show the economy dipped back into a contraction after a stronger than expected second quarter, and on Thursday the country will report on trade.

Marion Kohler, acting assistant governor of Australia’s central bank, speaks on Monday, and data Tuesday is likely to show business sentiment holding up better than that of households in Australia amid higher interest rates.

Across the Tasman Sea, Reserve Bank of New Zealand Assistant Governor Karen Silk is set to speak on the bank’s balance sheet on Tuesday.

Elsewhere in the region, Sri Lanka on Monday is likely to raise taxes in its budget to meet the conditions of the International Monetary Fund’s $3 billion bailout program, while India’s October inflation pace is expected to slow further toward the central bank’s target band.

The Philippines’ central bank will issue its latest policy decision on Thursday, while Malaysia reports on final third quarter GDP data on Friday.

- For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

UK data will be a highlight. Wage numbers on Tuesday may point to softening, while inflation the next day is likely to slow to a two-year low from a level that stands out as the fastest in the Group of Seven nations.

Both outcomes would support the view of Bank of England chief economist Huw Pill that further rate increases aren’t needed. Governor Andrew Bailey on Wednesday pushed against the prospect of early rate cuts — days before data that showed the economy stalled in the third quarter, though staved off a recession.

In Brussels, new European Union forecasts on Wednesday will show a revised outlook at a time the region could well be extending a contraction. The release will also feature fiscal projections, which will take on added significance given the reinstatement of the bloc’s 3% deficit rule in 2024.

Italy, in particular, is a concern for officials, not least after its government unveiled a looser fiscal stance. The country is on a negative outlook at the lowest rung of investment grade at Moody’s Investors Service, which has penciled in Friday for a possible update of that view.

Revised takes of euro-region GDP and inflation will also be published, along with industrial production for September.

Among a spate of European Central Bank speakers, President Christine Lagarde will draw attention with remarks at a conference on Friday.

Looking north, inflation in Sweden will focus investors on Tuesday. Riksbank officials may disregard a likely acceleration in the CPIF measure that they target.

In the east, third-quarter GDP releases will be a highlight. It’s a close call whether Hungary’s economy under Prime Minister Viktor Orban emerged from a year-long recession, while Poland will publish numbers too.

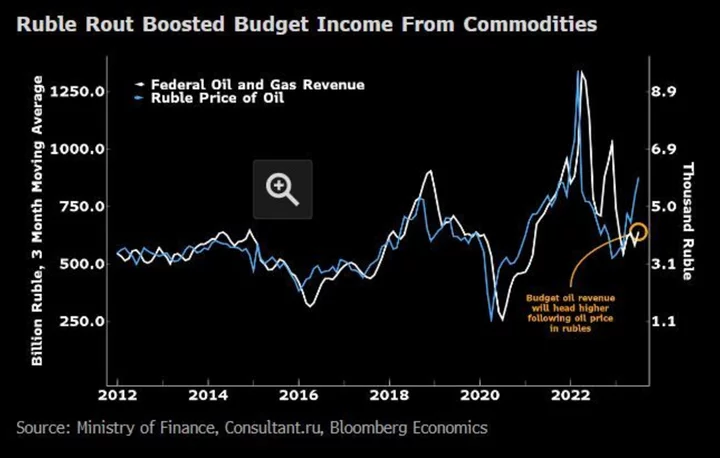

Russian data on Wednesday are likely to show the economy continued to rebound despite international sanctions over its invasion of Ukraine, and possibly expanded by more than 5% — the fastest pace since the war began.

In Africa, Ghanaian Finance Minister Ken Ofori-Atta will deliver his 2024 budget on Wednesday with plans expected to rein in debt and increase revenue as part of conditions for a $3 billion IMF bailout. Data the same day are expected to show inflation slowed for a third straight month in October to 36%.

In Nigeria, a continued slump in the naira will likely see yearly inflation quicken to more than 27% in October from 26.7% a month earlier.

Also on Wednesday, investors will get the first indication of how the war with Hamas is affecting prices in Israel. Analysts surveyed by Bloomberg see last month’s inflation rate dipping further, to 3.7%.

- For more, read Bloomberg Economics’ full Week Ahead for EMEA

Latin America

In the final economic release before Argentina elects a new president, government data will likely show that annual inflation jumped past 145% last month. Economists surveyed by the central bank see it surging anew in both November and December to end the year at 181%.

Chile’s central bank on Tuesday posts minutes of its Oct. 26 decision to slow the pace of easing. The board cited the deterioration of financial conditions globally and rise of global geopolitical uncertainty that’s undermining the peso.

Peru’s GDP-proxy data on Wednesday should confirm that the economy shrank for a third consecutive quarter in the three months through September as domestic demand remains weak and China’s struggles weigh on exports.

Brazil’s GDP-proxy data for September may show that growth sputtered amid a surprising 2023. While consumers in Latin America’s biggest economy are feeling the bite of double-digit rates, government spending, federal aid to lower income households and a tight labor market are helping to support demand.

The focus in Colombia will be on third-quarter output. Analysts see a rebound from the prior three months staving off a technical recession and forecast that only Brazil and Mexico among the region’s big economies will expand faster in 2023.

- For more, read Bloomberg Economics’ full Week Ahead for Latin America

--With assistance from Laura Dhillon Kane, Piotr Skolimowski, Monique Vanek, Paul Wallace, Robert Jameson, Yuko Takeo and Tony Halpin.