If they’d been offered today’s economy a year ago – with inflation downgraded from emergency to mere headache, still-low unemployment, and growth that’s slowed without stalling – the world’s top central bankers would’ve taken it like a shot.

That doesn’t mean anyone at Jackson Hole, where Federal Reserve chief Jerome Powell and his peers meet this week, is likely to declare mission accomplished.

One example of the fragile backdrop to this year’s gathering: Even in the US, which has the rosiest numbers among major economies, two-thirds of 602 respondents in Bloomberg’s latest Markets Live Pulse survey say the Fed has yet to conquer inflation.

Powell and co. can’t be sure they’ve raised interest rates high enough to tame prices. They’re even less clear about how long policy will have to stay tight –- increasingly the dominant question for financial markets.

“We could see ourselves in this 5+ percent benchmark risk-free rate environment for the foreseeable period of time – perhaps into mid-2024 or beyond,” says Jerome Schneider, head of short-term portfolio management and funding at Pacific Investment Management Co., which oversees $1.8 trillion in assets.

‘Pushed to the Brink’

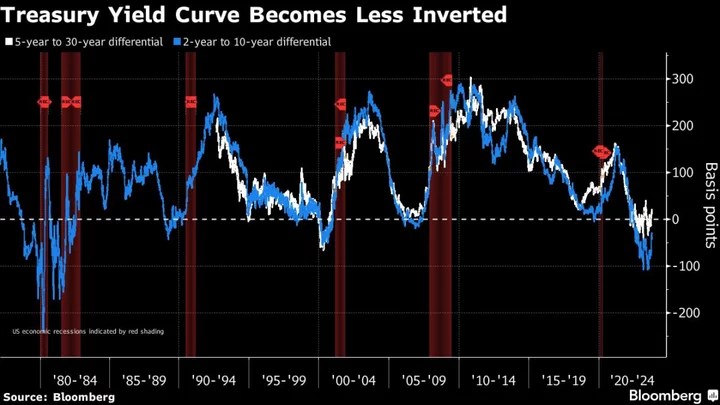

Global government bond yields have already surged to the highest in more than a decade – with rates on benchmark 10-year debt reaching as high as 4.33% this month in the US and 4.75% in the UK – on expectations that the Jackson Hole crew aren’t done hiking yet.

If those bets are on point, few corners of the financial world will escape the consequences.

“If markets think that rates will be higher for longer, fundamentally you would discount future profits more heavily, so you would have an adjustment in stock prices,” says Gian Maria Milesi-Ferretti, a senior fellow at the Brookings Institution and former deputy research director at the International Monetary Fund. Also, “you could have more firms pushed to the brink by an increase in debt servicing costs.”

Even without further hikes, the monetary medicine that central banks have already doled out could yet have the lagged effect of tipping economies into a slump, or blowing up some more banks.

About 80% of the MLIV Pulse respondents expect a euro-area recession in the coming year. Most forecasters are more optimistic than that – but Germany, Europe’s largest economy, already suffered a winter downturn and has little prospect of growth for the rest of the year.

For the US, the survey split exactly 50-50 on the chance of a downturn over the next 12 months. More than half of respondents said it’s financial-market turbulence that will likely prompt the next Fed rate cut, rather than labor-market weakness or easing inflation.

‘How Long?’

In the US, markets see a better-than even chance that central bank interest rates have already peaked. That’s not the case elsewhere.

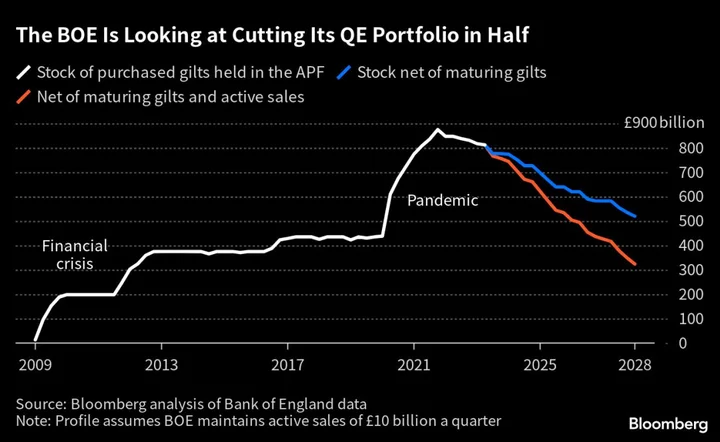

The UK has the worst of all worlds on inflation - with high energy prices like continental Europe, and rising wages like the US - meaning the Bank of England has more work to do. In Japan, new central bank governor Kazuo Ueda shows signs of shifting back into the mainstream of monetary policy a little faster than expected.

After the European Central Bank’s last hike in July, President Christine Lagarde said the region’s near-term economic outlook had deteriorated, and subsequent ECB research suggests that underlying inflation may have peaked. Lagarde’s speech in Jackson Hole may offer early clues following the European summer break about whether policymakers are leaning toward another rate increase, or a pause.

For both the Fed and the ECB, “how long” is on track to replace “how high” as the key question.

“That’s really what I think Chair Powell will focus on” when he addresses the Jackson Hole meeting, Lindsey Piegza — chief economist at Stifel Financial Corp. — told Bloomberg Television last week. “How long will the Fed need to keep rates at that elevated level?”

At the ECB, Executive Board member Fabio Panetta — one of the bank’s doves — said this month that “persistence is becoming as important as the level of our policy rates,” echoing other European monetary heavyweights. The thinking is that taking borrowing costs to less lofty heights, but keeping them there for longer, could minimize damage to the economy and lift the odds of the soft landing that central bankers everywhere are chasing.

‘Things Look Better’

Either way, a cut in European borrowing costs isn’t in the cards anytime soon. About 30% of MLIV survey participants said that won’t happen before at least the fourth quarter of next year, compared with just 21% who said the same about the Fed.

Of course, much of this debate is based on textbook monetary-policy calculations – which could easily get blown off course.

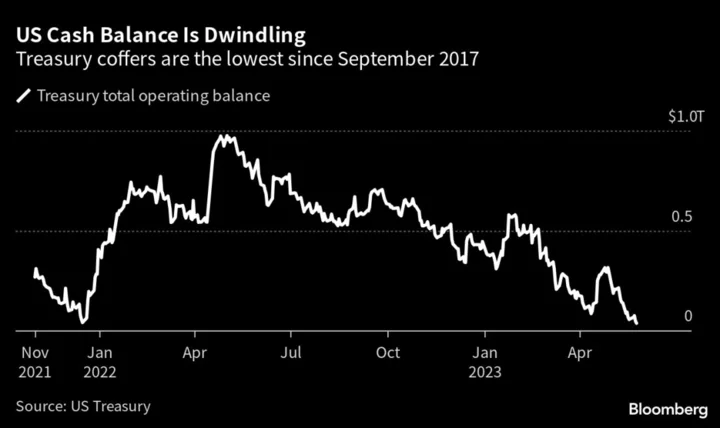

There’s growing alarm, for example, that a China downturn will send shockwaves through the world economy. Russia’s war in Ukraine still has the potential to trigger commodity turmoil. Unprecedented US budget deficits are starting to worry investors in the $25 trillion Treasury market, and Europe just got hit by another energy-price spike.

“The economy has surprised on the upside and inflation on the downside,” says Milesi-Ferretti. “Things obviously look much better than they did even a few months ago. But we really don’t know.”

The MLIV Pulse survey of Bloomberg News readers on the terminal and online is conducted weekly by Bloomberg’s Markets Live team, which also runs the MLIV blog. This week, the poll focuses on China. If China sells US Treasuries to fund its currency intervention, will it that drive 10-year US yields higher? Share your views.

Author: Liz Capo McCormick, Jana Randow and Jonnelle Marte